New Zealand Milk Production Update – Oct ’21

Executive Summary

New Zealand milk production figures provided by Dairy Companies Association of New Zealand (DCANZ) were recently updated with values spanning through Sep ’21. Highlights from the updated report include:

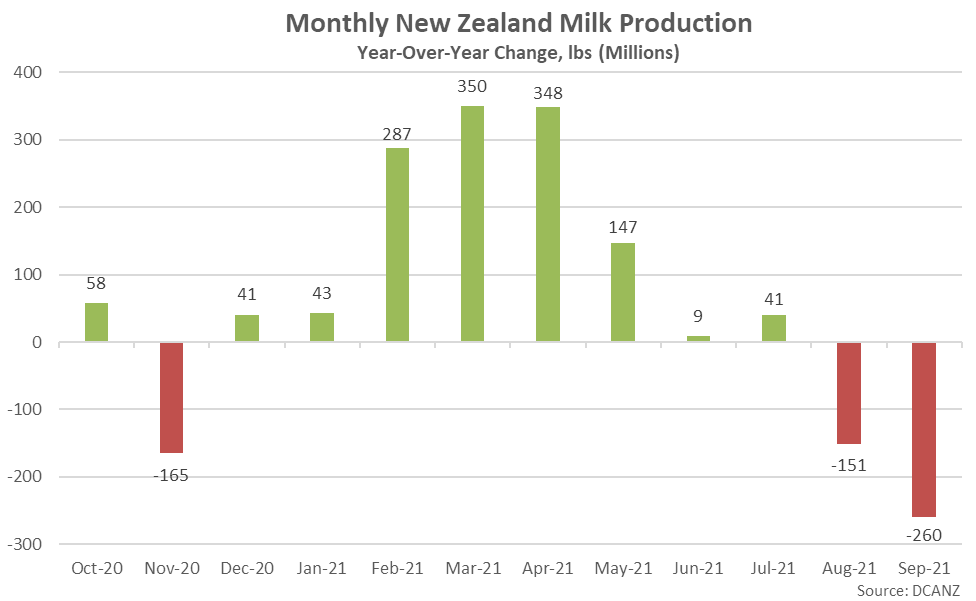

- New Zealand milk production volumes declined 4.4% on a YOY basis throughout Sep ’21, reaching a four year low seasonal level. The YOY decline in New Zealand milk production volumes was the largest experienced throughout the past 29 months on an absolute basis.

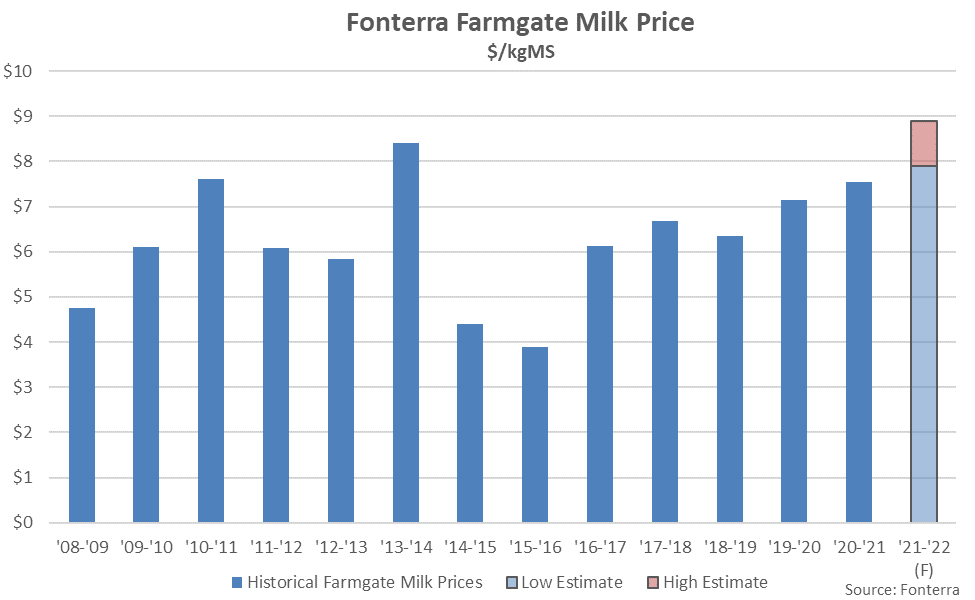

- Fonterra’s ’21-’22 farmgate milk price forecast of $7.90-$8.90/kgMS is currently 11.4% above the seven year high level experienced throughout the previous season at the midpoint of the forecast and is on pace to tie the record high level experienced throughout the ’13-’14 production season.

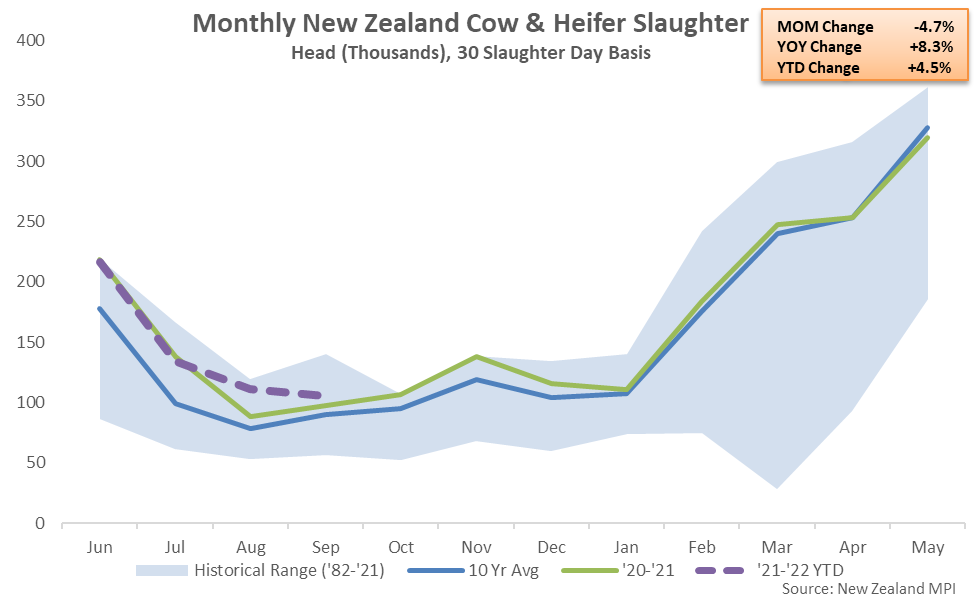

- New Zealand cow & heifer slaughter rates increased 8.3% on a YOY basis during Sep ’21 when normalizing for slaughter days, remaining at a six year high seasonal level for the second consecutive month.

Additional Report Details

Milk Production

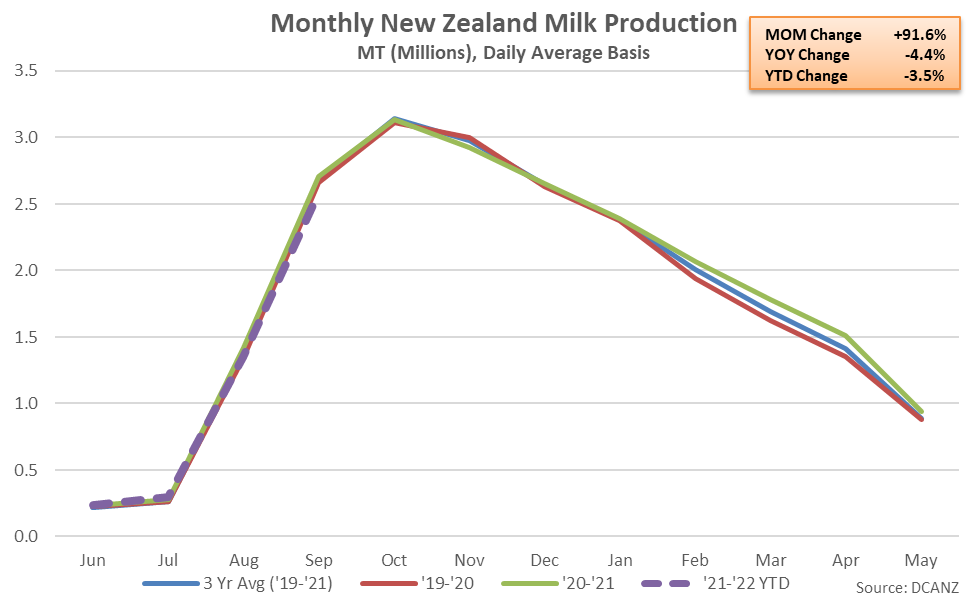

According to Dairy Companies Association of New Zealand (DCANZ), Sep ’21 New Zealand milk production volumes increased seasonally to a nine month high level but finished 4.4% below previous year levels. New Zealand milk production volumes finished at a four year low seasonal level for the month of September. On a milk-solids basis, production declined 4.0% YOY, also reaching a four year low seasonal level.

The Sep ’21 YOY decline in New Zealand milk production volumes was the second experienced in a row and the largest experienced throughout the past 29 months on an absolute basis. New Zealand milk production volumes had finished above previous year levels over eight consecutive months through Jul ’21, prior to declining on a YOY basis over the two most recent months of available data.

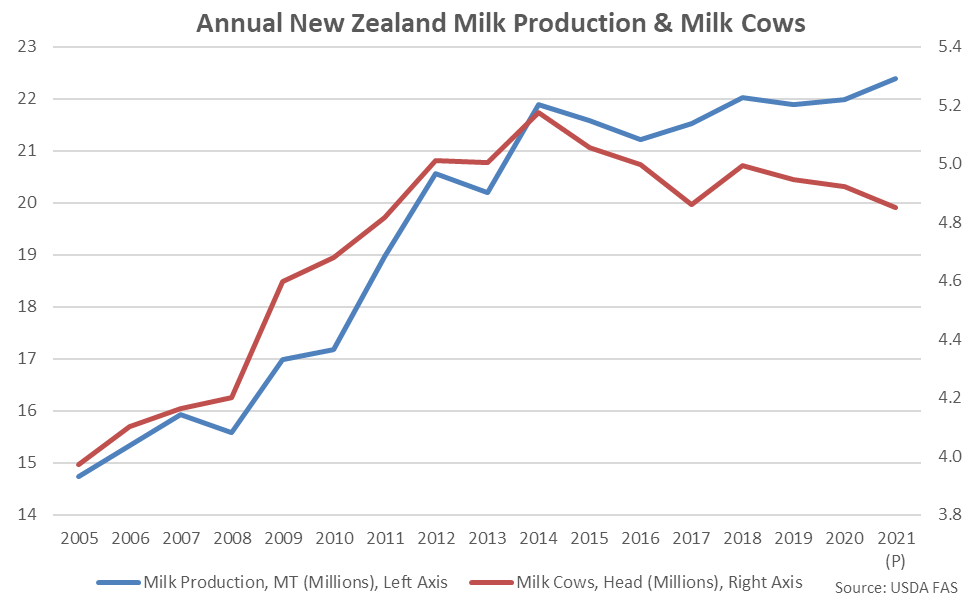

‘20-’21 annual New Zealand milk production volumes increased by 3.0% on a YOY basis, reaching a record high annual level. The 3.0% annual growth rate was the largest experienced throughout the past seven years. ‘21-’22 YTD New Zealand milk production volumes have declined by 3.5% on a YOY basis throughout the first third of the production season, however.

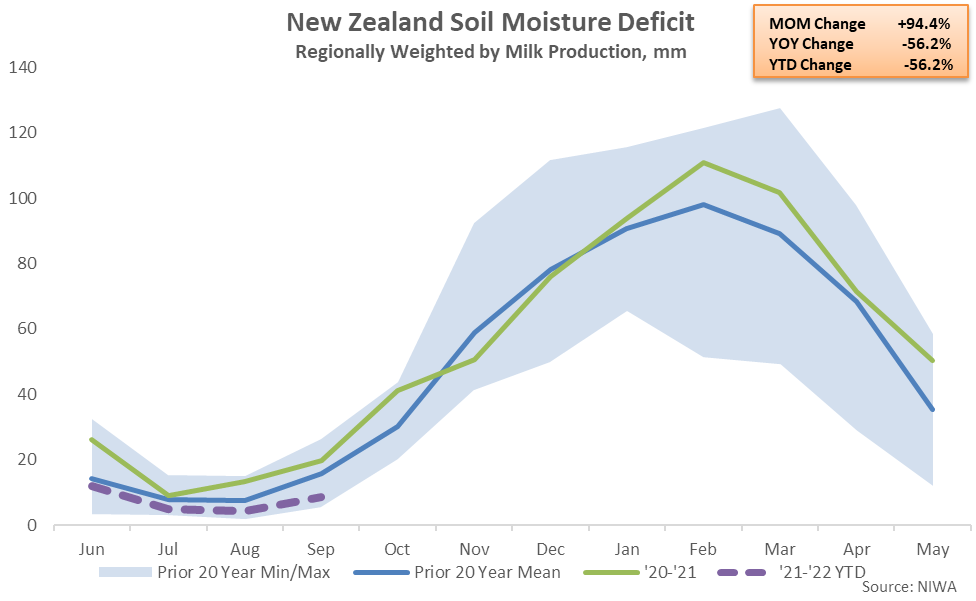

Rainfall & Soil Moisture Deficits

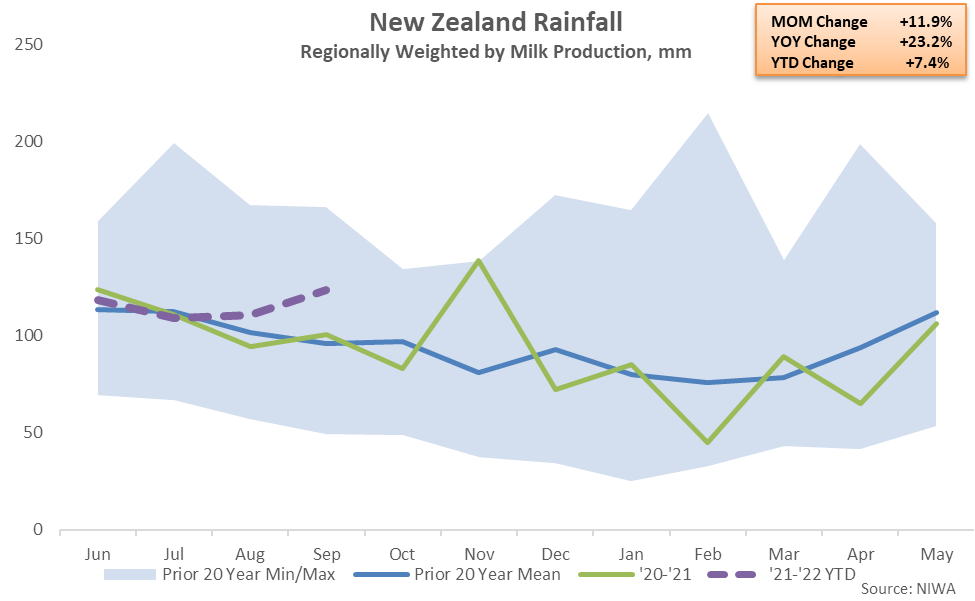

New Zealand rainfall remained above long-term historical seasonal levels throughout Sep ’21 when regionally weighted by milk production volumes, reaching a four year high seasonal level and the second highest seasonal level experienced throughout the past 11 years. Rainfall levels finished 23.2% above previous year levels and 28.7% above 20 year average seasonal levels for the month of September. Total New Zealand rainfall levels have finished 7.4% above previous year levels throughout the first third of the ’21-’22 production season.

New Zealand soil moisture deficits remained below previous year levels for the ninth consecutive month throughout Sep ’21 when regionally weighted by milk production volumes. New Zealand soil moisture deficits remained at a four year low seasonal level for the month of September.

Farmgate Milk Prices

Fonterra’s final ’20-’21 farmgate milk price of $7.54/kgMS reached a seven year high level on strong Chinese and Southeast Asian powder demand. Fonterra raised their ’21-’22 farmgate milk price forecast to a value of $7.90-$8.90/kgMS in late Oct ’21, up $0.40/kgMS, or 4.8%, from the previous forecast. The midpoint of the ’21-’22 farmgate milk price forecast is currently 11.4% above previous year levels and is on pace to tie the record high level experienced throughout the ’13-’14 production season.

Cow & Heifer Slaughter

New Zealand cow & heifer slaughter rates increased 8.3% on a YOY basis during Sep ’21 when normalizing for slaughter days, remaining at a six year high seasonal level for the second consecutive month. Sep ’21 dairy cow & heifer slaughter, which has more limited historical data available, finished 8.4% above previous year levels, also reaching a six year high seasonal level.

’20-’21 annual New Zealand cow & heifer slaughter finished 4.0% above the previous year, reaching a five year high level and the third highest annual figure on record. ’21-’22 YTD New Zealand cow & heifer slaughter rates have increased by an additional 4.5% throughout the first third of the production season and are on pace to reach a record high annual level.

New Zealand milk production volumes increased at a compound annual growth rate of 4.2% over the ten year period ending during the ’14-’15 record production season but growth has moderated over more recent years as farmgate milk prices declined from the ’13-’14 record high levels and the New Zealand milk cow herd was reduced. USDA is projecting the New Zealand milk cow herd will decline 1.5% on a YOY basis throughout 2021, reaching a ten year low level.