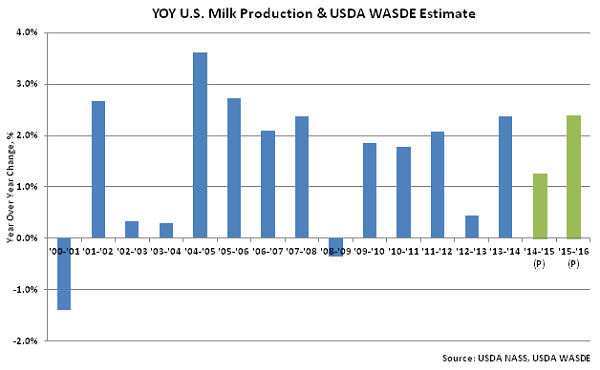

2015 U.S. Milk Production Projected Lowered For Seventh Consecutive…

According to the May USDA World Agricultural Supply and Demand Estimate (WASDE) report, 2015 projected U.S. milk production was lowered to 208.6 billion lbs, down 1.4 billion lbs from the previous report. Production was revised lower as drought in the West has impacted milk per cow and growth in the cow herd is expected to be slower than previously anticipated. 2015 projected U.S. milk production has been revised lower in each of the last seven WASDE reports. 2015 projected production of 208.6 billion lbs equates to a 1.3% YOY increase from 2014 production of 206.0 billion lbs. The projected 1.3% YOY increase in milk production would be less than the three year average growth rate of 1.6%.

USDA released their 2016 projected U.S. milk production figure for the first time in the May WASDE report, with 2016 projected production of 213.6 billion lbs up 2.4% from the 2015 projected production of 208.6 billion lbs. Milk production for 2016 is forecast higher as improved forage availability and moderate feed costs are expected to support gains in milk per cow, while cow numbers were also forecast slightly higher. The 2.4% increase in YOY milk production would be the largest in ten years.

Export forecasts on a fat basis were raised for 2015 on strong March export figures while export forecasts on a skim-solids basis were raised on higher nonfat dry milk (NFDM) and lactose shipments. Fat and skim-solids imports for 2015 were raised on strong cheese demand. Commercial exports on both a fat and skim-solids basis were forecast higher for 2016 as a resumption of normal trade patterns is expected. Imports for 2016 were forecast lower as domestic production increases and demand from competing importers remains high.

Cheese, NFDM and whey prices were forecast lower for 2015 on weak demand, but the 2015 butter forecasted price was raised on strong demand. The 2015 Class III price estimate of $16.05-$16.55/cwt was reduced by $0.15/cwt while the 2015 Class IV price estimate of $14.35-$14.95/cwt was lowered by $0.10/cwt. For 2016, cheese, NFDM and whey prices were forecasted higher on stronger domestic demand and exports, but butter prices were forecasted lower as strong NFDM demand is expected to support relatively high levels of butter production. The initial 2016 Class III price forecast of $16.20-$17.20/cwt was 2.5% above the 2015 forecasted level while the initial 2016 Class IV price forecast of $15.60-$16.70/cwt was 10.2% above the 2015 forecasted level.

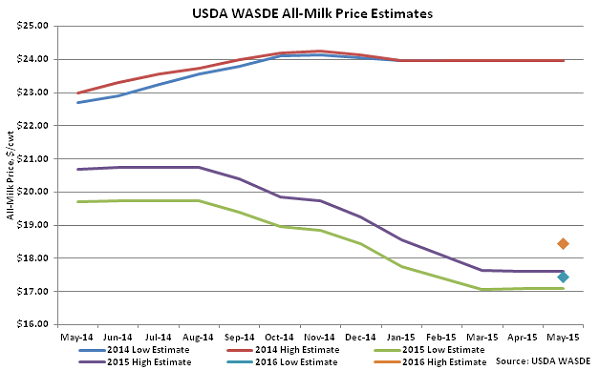

As shown in the chart below, the 2015 All-Milk price is expected to be well below previous year price levels, at a range of $17.10-$17.60/cwt, unchanged from last month and 27.6% below the 2014 average All-Milk price of $23.98/cwt. The initial 2016 All-Milk price forecast of $17.45-$18.45/cwt remains significantly below 2014 levels but was 3.5% higher than 2015 forecast prices.

Export forecasts on a fat basis were raised for 2015 on strong March export figures while export forecasts on a skim-solids basis were raised on higher nonfat dry milk (NFDM) and lactose shipments. Fat and skim-solids imports for 2015 were raised on strong cheese demand. Commercial exports on both a fat and skim-solids basis were forecast higher for 2016 as a resumption of normal trade patterns is expected. Imports for 2016 were forecast lower as domestic production increases and demand from competing importers remains high.

Cheese, NFDM and whey prices were forecast lower for 2015 on weak demand, but the 2015 butter forecasted price was raised on strong demand. The 2015 Class III price estimate of $16.05-$16.55/cwt was reduced by $0.15/cwt while the 2015 Class IV price estimate of $14.35-$14.95/cwt was lowered by $0.10/cwt. For 2016, cheese, NFDM and whey prices were forecasted higher on stronger domestic demand and exports, but butter prices were forecasted lower as strong NFDM demand is expected to support relatively high levels of butter production. The initial 2016 Class III price forecast of $16.20-$17.20/cwt was 2.5% above the 2015 forecasted level while the initial 2016 Class IV price forecast of $15.60-$16.70/cwt was 10.2% above the 2015 forecasted level.

As shown in the chart below, the 2015 All-Milk price is expected to be well below previous year price levels, at a range of $17.10-$17.60/cwt, unchanged from last month and 27.6% below the 2014 average All-Milk price of $23.98/cwt. The initial 2016 All-Milk price forecast of $17.45-$18.45/cwt remains significantly below 2014 levels but was 3.5% higher than 2015 forecast prices.

Export forecasts on a fat basis were raised for 2015 on strong March export figures while export forecasts on a skim-solids basis were raised on higher nonfat dry milk (NFDM) and lactose shipments. Fat and skim-solids imports for 2015 were raised on strong cheese demand. Commercial exports on both a fat and skim-solids basis were forecast higher for 2016 as a resumption of normal trade patterns is expected. Imports for 2016 were forecast lower as domestic production increases and demand from competing importers remains high.

Cheese, NFDM and whey prices were forecast lower for 2015 on weak demand, but the 2015 butter forecasted price was raised on strong demand. The 2015 Class III price estimate of $16.05-$16.55/cwt was reduced by $0.15/cwt while the 2015 Class IV price estimate of $14.35-$14.95/cwt was lowered by $0.10/cwt. For 2016, cheese, NFDM and whey prices were forecasted higher on stronger domestic demand and exports, but butter prices were forecasted lower as strong NFDM demand is expected to support relatively high levels of butter production. The initial 2016 Class III price forecast of $16.20-$17.20/cwt was 2.5% above the 2015 forecasted level while the initial 2016 Class IV price forecast of $15.60-$16.70/cwt was 10.2% above the 2015 forecasted level.

As shown in the chart below, the 2015 All-Milk price is expected to be well below previous year price levels, at a range of $17.10-$17.60/cwt, unchanged from last month and 27.6% below the 2014 average All-Milk price of $23.98/cwt. The initial 2016 All-Milk price forecast of $17.45-$18.45/cwt remains significantly below 2014 levels but was 3.5% higher than 2015 forecast prices.