Grain & Oilseeds WASDE Update – Sep ’21

Corn – U.S. and Global Ending Stocks Above Private Estimates

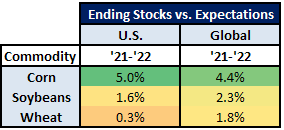

- ’21-’22 U.S. ending stocks of 1.408 billion bushels above expectations

- ’21-’22 global ending stocks of 297.6 million MT above expectations

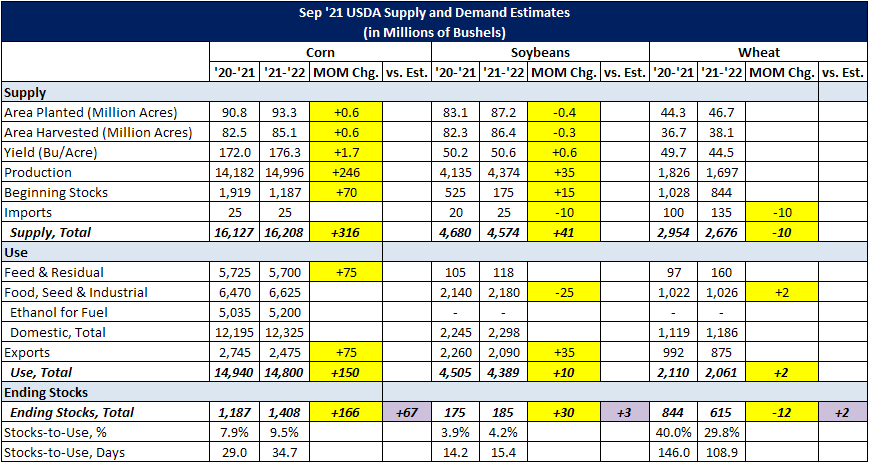

The ’21-’22 U.S. corn supply projection was raised from the previous month on a 600,000 acre increase in area harvested, coupled with a 1.7 bu/acre increase in yields and higher beginning stocks. The ’21-’22 corn yield projection of 176.3 bu/acre finished 0.4% above expectations of a 175.6 bu/acre yield. The U.S. corn demand projection was also raised from the previous month on increases in feed & residual usage and exports, offsetting nearly half of the projected increase in supply. ’21-’22 projected U.S. corn ending stocks of 1.408 billion bushels, or 34.7 days of use, finished 13.4% above the previous month and 5.0% above expectations. The ’21-’22 global corn ending stock projection finished 4.6% above the previous month and 4.4% above expectations, primarily on increases in Chinese production and beginning stocks, coupled with the increase in U.S. production.

Soybeans – U.S. and Global Ending Stocks Above Private Estimates

- ’21-’22 U.S. ending stocks of 185 million bushels above expectations

- ’21-’22 global ending stocks of 98.9 million MT above expectations

The ’21-’22 U.S. soybean supply projection was raised from the previous month as a 0.6 bu/acre increase in yields more than offset a 300,000 acre decline in area harvested. Beginning stocks were also raised from the previous month, although the increase was largely offset by a reduction in projected imports. The ’21-’22 soybean yield projection of 50.6 bu/acre finished 0.6% above expectations of a 50.3 bu/acre yield. The U.S. soybean demand projection was raised slightly from the previous month as an increase in projected exports more than offset lower projected food, seed & industrial usage. ’21-’22 projected U.S. soybean ending stocks of 185 million bushels, or 15.4 days of use, finished 19.4% above the previous month and 1.6% above expectations. The ’21-’22 global soybean ending stock projection finished 2.8% above the previous month and 2.3% above expectations, largely on an increase in Chinese beginning stocks.

Soybean Complex – U.S. Oil Stocks Raised, U.S. Meal Stocks Unchanged

The ’21-’22 U.S. soybean oil ending stock projection was raised from the previous month as reductions in biofuel and export demand more than offset higher supplies and food, feed & other industrial usage. Globally, ’21-’22 soybean oil ending stocks were reduced from the previous month on widespread declines in projected beginning stocks.

The ’21-’22 U.S. soybean meal ending stock projection was unchanged from the previous month as a reduction in production was offset by lower projected domestic usage. Globally, ’21-’22 global soybean meal ending stocks were reduced from the previous month as a reduction in Argentine beginning stocks more than offset an increase in Brazilian beginning stocks.

Wheat – U.S. and Global Ending Stocks Above Private Estimates

- ’21-’22 U.S. ending stocks of 615 million bushels above expectations

- ’21-’22 global ending stocks of 283.2 million MT slightly above expectations

The ’21-’22 U.S. wheat supply projection was reduced slightly from the previous month on a reduction in imports while the U.S. wheat demand projection was largely unchanged from the previous month. ’21-’22 projected U.S. wheat ending stocks of 615 million bushels, or 108.9 days of use, finished 1.9% below the previous month but 0.3% above expectations. The ’21-’22 global wheat ending stock projection finished 1.5% above the previous month and 1.8% above expectations, primarily on increases in Indian production and Canadian and European Union beginning stocks.

Ending Stocks vs. Expectations Summary

Overall, ’21-’22 projected domestic corn ending stocks finished most significantly above expectations, followed by global corn ending stocks, global soybean ending stocks, global wheat ending stocks, domestic soybean ending stocks and domestic wheat ending stocks.