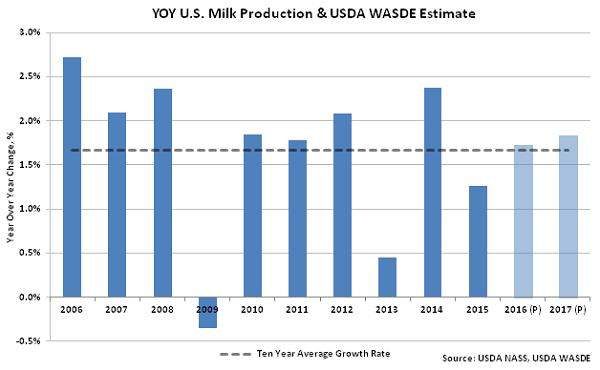

U.S. Milk Production Projected Higher – Sep ’16

According to the September USDA World Agricultural Supply and Demand Estimate (WASDE) report, the 2016 U.S. milk production projection was raised for the first time in three months as the cow inventory appears to have steadied due to expected improvements in returns. 2016 projected milk production of 212.2 billion pounds was raised by 0.1 billion pounds but remained at the second lowest figure experienced throughout the past five months. 2016 projected production translates to a 1.7% increase from the 2015 production levels, which would be consistent with the ten year average growth rate. Projected milk production is expected to increase an additional 1.8% throughout 2017, finishing at an estimated level of 216.1 billion pounds, up 0.3 billion pounds from the previous month’s projection. Higher milk per cow yields contributed to the increase in the 2017 milk production projection.

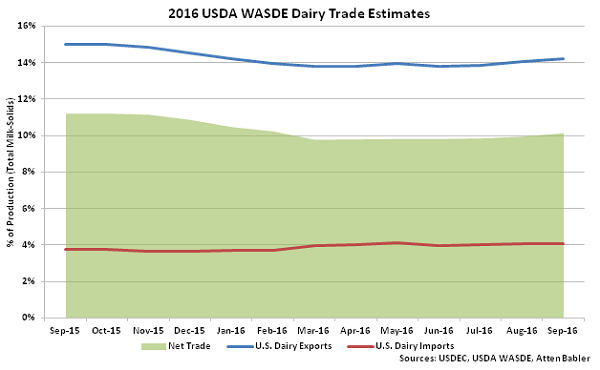

Export forecasts were raised for both 2016 and 2017 on a fat basis as cheese and cream export volumes have remained firm throughout 2016 and whole milk powder (WMP) exports are expected to continue to strengthen into 2017. Export volumes were also raised on a skim-solids basis for both 2016 and 2017 on higher WMP and whey sales. The 2016 projected dairy export volumes translated to 14.2% of total U.S. milk solids production while import volumes were equivalent to 4.1% of total U.S. milk solids production. U.S. net dairy trade projections increased slightly, finishing at a seven month high of 10.1% during the September report. Despite higher export forecasts, 2016 ending stocks were forecast higher on both a fat and skim-solids basis as butter and cheese stocks remain high.

Export forecasts were raised for both 2016 and 2017 on a fat basis as cheese and cream export volumes have remained firm throughout 2016 and whole milk powder (WMP) exports are expected to continue to strengthen into 2017. Export volumes were also raised on a skim-solids basis for both 2016 and 2017 on higher WMP and whey sales. The 2016 projected dairy export volumes translated to 14.2% of total U.S. milk solids production while import volumes were equivalent to 4.1% of total U.S. milk solids production. U.S. net dairy trade projections increased slightly, finishing at a seven month high of 10.1% during the September report. Despite higher export forecasts, 2016 ending stocks were forecast higher on both a fat and skim-solids basis as butter and cheese stocks remain high.

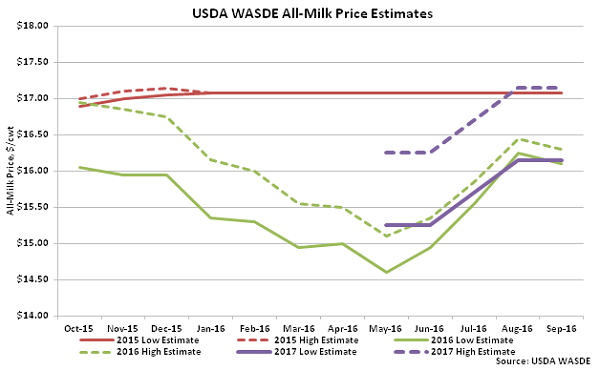

Butter and cheese prices were lowered for both 2016 and 2017 as supplies remain high, however prices for nonfat dry milk (NFDM) and dry whey were forecast higher as global supplies have tightened on strengthening demand. The Class III price forecast was lowered by $0.05/cwt, finishing at $14.75-$14.95/cwt, as reductions in forecasted cheese prices more than offset the increase in forecasted dry whey prices, while the 2016 Class IV price forecast was lowered by $0.10/cwt, finishing at $13.65-$13.95/cwt, as the lower projected butter price more than offset the higher NFDM price. The 2016 All-Milk price forecast of $16.10-$16.30/cwt was lowered by $0.15/cwt, finishing 5.2% below 2015 price levels. For 2017, the projected price of NFDM was raised, offsetting projected declines in butter and cheese prices from the previous month. The 2017 projected All-Milk price of $16.15-$17.15/cwt was unchanged, finishing 2.8% above 2016 price levels.

Butter and cheese prices were lowered for both 2016 and 2017 as supplies remain high, however prices for nonfat dry milk (NFDM) and dry whey were forecast higher as global supplies have tightened on strengthening demand. The Class III price forecast was lowered by $0.05/cwt, finishing at $14.75-$14.95/cwt, as reductions in forecasted cheese prices more than offset the increase in forecasted dry whey prices, while the 2016 Class IV price forecast was lowered by $0.10/cwt, finishing at $13.65-$13.95/cwt, as the lower projected butter price more than offset the higher NFDM price. The 2016 All-Milk price forecast of $16.10-$16.30/cwt was lowered by $0.15/cwt, finishing 5.2% below 2015 price levels. For 2017, the projected price of NFDM was raised, offsetting projected declines in butter and cheese prices from the previous month. The 2017 projected All-Milk price of $16.15-$17.15/cwt was unchanged, finishing 2.8% above 2016 price levels.

Export forecasts were raised for both 2016 and 2017 on a fat basis as cheese and cream export volumes have remained firm throughout 2016 and whole milk powder (WMP) exports are expected to continue to strengthen into 2017. Export volumes were also raised on a skim-solids basis for both 2016 and 2017 on higher WMP and whey sales. The 2016 projected dairy export volumes translated to 14.2% of total U.S. milk solids production while import volumes were equivalent to 4.1% of total U.S. milk solids production. U.S. net dairy trade projections increased slightly, finishing at a seven month high of 10.1% during the September report. Despite higher export forecasts, 2016 ending stocks were forecast higher on both a fat and skim-solids basis as butter and cheese stocks remain high.

Butter and cheese prices were lowered for both 2016 and 2017 as supplies remain high, however prices for nonfat dry milk (NFDM) and dry whey were forecast higher as global supplies have tightened on strengthening demand. The Class III price forecast was lowered by $0.05/cwt, finishing at $14.75-$14.95/cwt, as reductions in forecasted cheese prices more than offset the increase in forecasted dry whey prices, while the 2016 Class IV price forecast was lowered by $0.10/cwt, finishing at $13.65-$13.95/cwt, as the lower projected butter price more than offset the higher NFDM price. The 2016 All-Milk price forecast of $16.10-$16.30/cwt was lowered by $0.15/cwt, finishing 5.2% below 2015 price levels. For 2017, the projected price of NFDM was raised, offsetting projected declines in butter and cheese prices from the previous month. The 2017 projected All-Milk price of $16.15-$17.15/cwt was unchanged, finishing 2.8% above 2016 price levels.