Dairy WASDE Update – Jun ’21

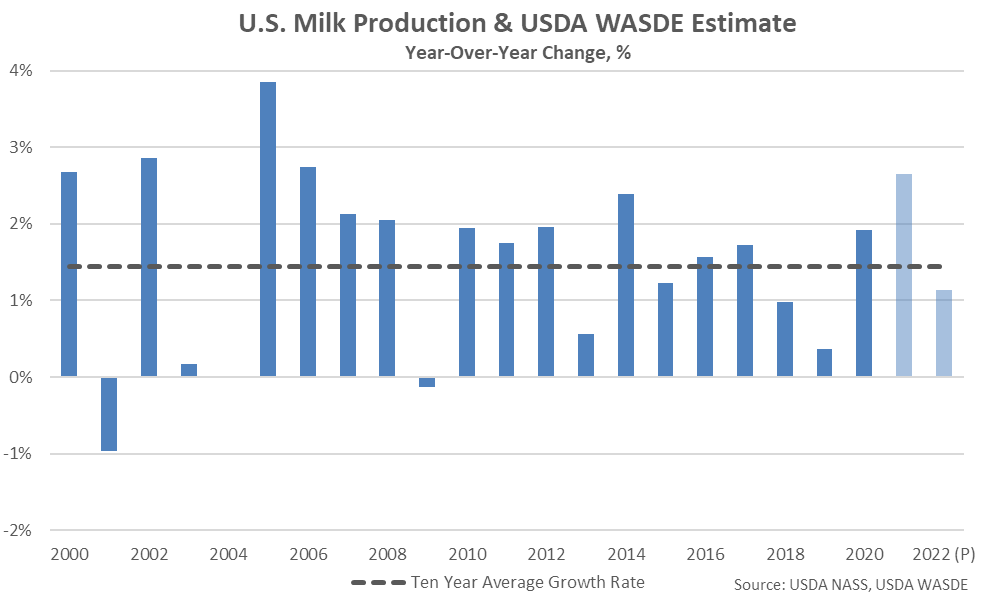

According to the June USDA World Agricultural Supply and Demand Estimate (WASDE) report, the 2021 milk production projection was raised six million pounds from the previous month on higher than expected dairy cow numbers. 2021 projected milk production equates to a 2.7% YOY increase from 2020 levels, which would be the largest growth rate experienced throughout the past 15 years.

U.S. milk production volumes are expected to increase by an additional 1.1% throughout 2022 as higher forecasted cow numbers are carried forward.

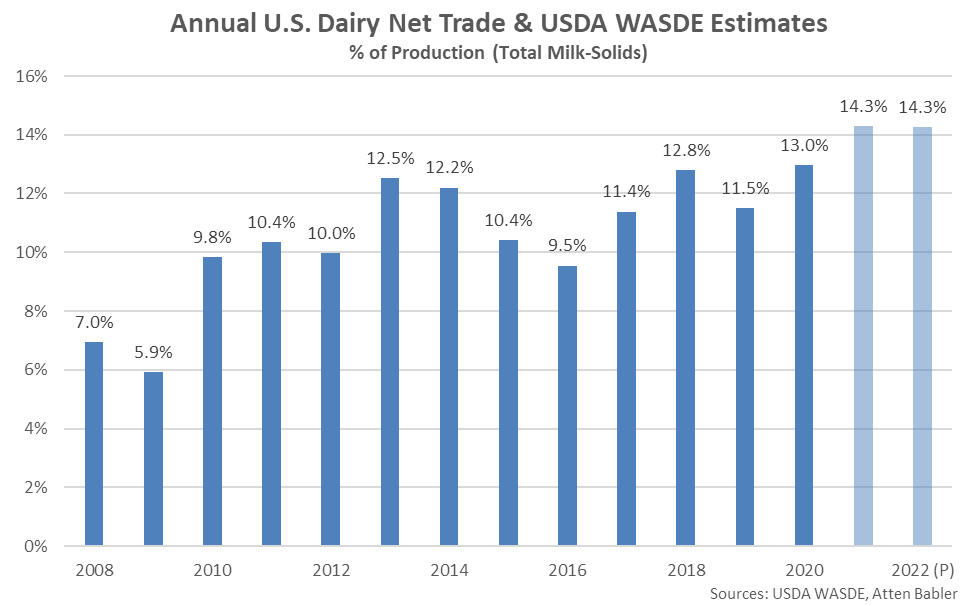

2021 dairy export forecasts were raised on both a milk-fat and skim-solids basis on higher expected exports of butterfat-containing products, cheese, whey and lactose. 2021 dairy import forecasts were reduced on a milk-fat basis on lower expected imports of butterfat containing products while remaining unchanged on a skim-solids basis.

The 2022 dairy exports forecast was raised on a skim-solids basis on an expected increase in whey demand while remaining unchanged on a milk-fat basis. 2022 dairy import forecasts were unchanged from the previous month on both a milk-fat and skim-solids basis.

2022 projected dairy export volumes translated to 17.7% of total U.S. milk solids production, down slightly from the record high level projected throughout the previous year, while import volumes were equivalent to 3.4% of total U.S. milk solids production, on pace to reach an eight year low level. 2022 net dairy trade is projected to remain at a record high level, unchanged from the previous year.

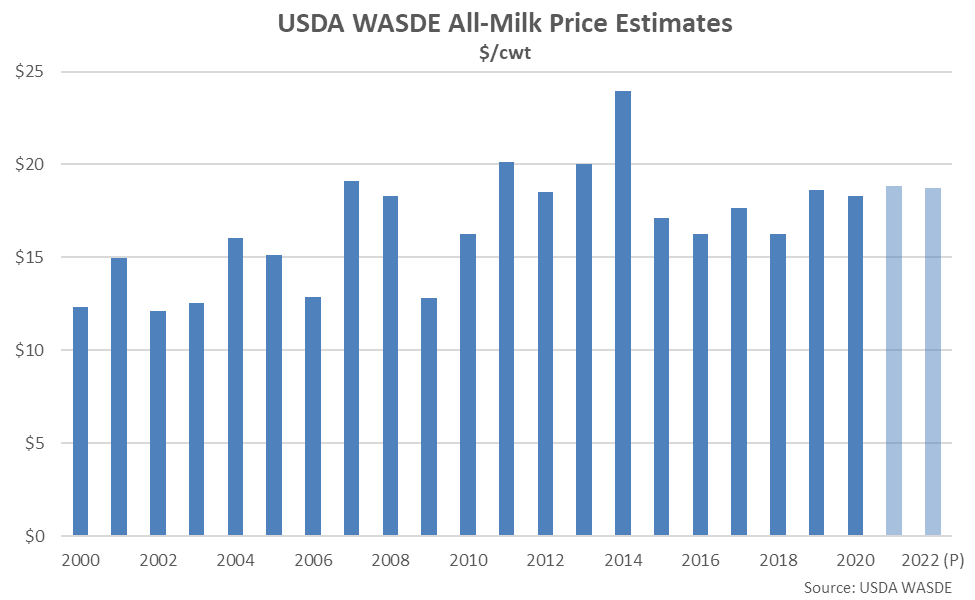

2021 butter, dry whey and nonfat dry milk price forecasts were raised from the previous month on recent price strength and stronger than anticipated demand, while cheese prices were reduced on relatively large stocks and current prices. The 2021 Class III milk price forecast of $17.45/cwt was reduced $0.25/cwt from the previous forecast, finishing 3.9% below the previous year price level. The 2021 Class IV milk price forecast of $15.85/cwt was raised $0.10/cwt from the previous forecast, finishing 17.5% above the previous year price level. The 2021 All-Milk price forecast of $18.85/cwt was reduced $0.10/cwt from the previous forecast but remained 2.9% above the 2020 price level.

2022 butter, dry whey and nonfat dry milk price forecasts were raised from the previous month while the cheese price was unchanged. The 2022 Class III milk price forecast of $17.15/cwt was raised $0.30/cwt from the previous forecast but remained 1.7% below the previous year’s projected price level. The 2022 Class IV milk price forecast of $15.95/cwt was raised $0.25/cwt from the previous forecast while finishing 0.6% above the previous year’s projected price level. The 2022 All-Milk price forecast of $18.75/cwt was raised $0.25/cwt from the previous month but remained 0.5% below the previous year’s projected price level.