Grain & Oilseeds WASDE Update – Apr ’22

Corn – U.S. and Global Ending Stocks Above Private Estimates

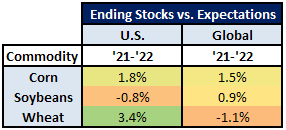

- ’21-’22 U.S. ending stocks of 1.44 billion bushels above expectations

- ’21-’22 global ending stocks of 305.5 million MT above expectations

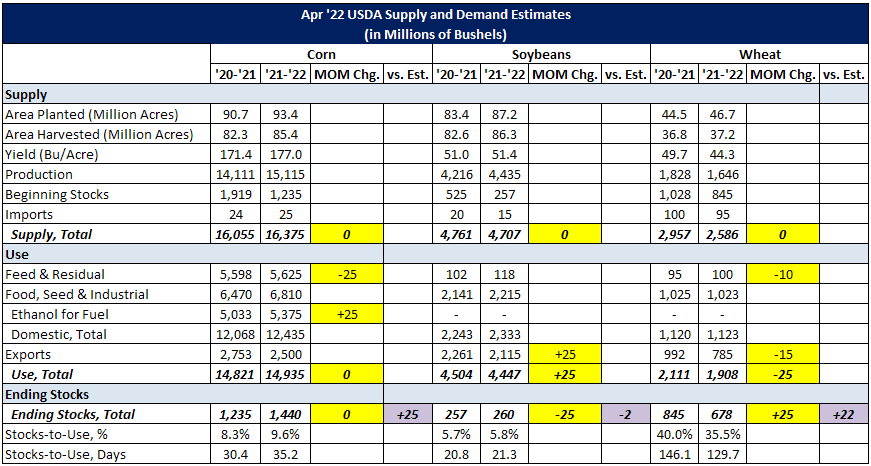

The ’21-’22 U.S. corn supply projection remained unchanged from the previous month while the demand projection was also unchanged as an expected increase in ethanol demand offset lower expected feed & residual usage. ’21-’22 projected U.S. corn ending stocks of 1.44 billion bushels, or 35.2 days of use, finished 1.8% above expectations.

The ’21-’22 global corn ending stock projection finished 1.5% above the previous month and 1.5% above expectations. Ukrainian and European Union corn stocks were revised most significantly above previous month projections. Lower Ukrainian corn exports are projected to more than offset higher domestic feed usage while European Union production and beginning stocks were revised higher. The April WASDE report represented an ongoing assessment of the short-term impacts of Russia’s recent military action in Ukraine. The USDA noted the situation significantly increased uncertainty of agricultural supply and demand conditions in the region and globally.

Soybeans – U.S. and Global Ending Stocks Mixed vs. Private Estimates

- ’21-’22 U.S. ending stocks of 260 million bushels slightly below expectations

- ’21-’22 global ending stocks of 89.6 million MT slightly above expectations

The ’21-’22 U.S. soybean supply projection remained unchanged from the previous month while the U.S. soybean demand projection was raised slightly on higher expected exports. ’21-’22 projected U.S. soybean ending stocks of 260 million bushels, or 21.3 days of use, finished 8.8% below the previous month and 0.8% below expectations.

The ’21-’22 global soybean ending stock projection finished 0.4% below the previous month but remained 0.9% above expectations. U.S. and Argentine soybean stocks were revised most significantly lower.

Soybean Complex – U.S. Oil Stocks Lower, Meal Stocks Unchanged

The ’21-’22 U.S. soybean oil ending stock projection was reduced from the previous month on an increase in expected exports. Globally, the ’21-’22 soybean oil ending stock projection was largely unchanged from the previous month.

The ’21-’22 U.S. soybean meal ending stock projection remained unchanged from the previous month as lower expected production and exports were offset by higher expected domestic disappearance and imports. Globally, the ’21-’22 soybean meal ending stock projection was raised from the previous month, led by increases in European Union beginning stocks.

Wheat – U.S. and Global Ending Stocks Mixed vs. Private Estimates

- ’21-’22 U.S. ending stocks of 678 million bushels above expectations

- ’21-’22 global ending stocks of 278.4 million MT below expectations

The ’21-’22 U.S. wheat supply projection remained unchanged from the previous month while the U.S. wheat demand projection was reduced on lower expected exports and feed & residual usage. ’21-’22 projected U.S. wheat ending stocks of 678 million bushels, or 129.7 days of use, finished 3.8% above the previous month and 3.4% above expectations.

The ’21-’22 global wheat ending stock projection finished 1.1% below the previous month and 1.1% below expectations as a decline in Indian ending stocks more than offset an increase in European Union ending stocks. Indian wheat ending stocks were revised lower largely on an increase in domestic usage while European Union wheat ending stocks were revised higher largely on a decline in exports.

Ending Stocks vs. Expectations Summary

Overall, ’21-’22 projected domestic wheat ending stocks finished most significantly above expectations, followed by domestic corn ending stocks, global corn ending stocks and global soybean ending stocks. Global wheat ending stocks finished below expectations, followed by domestic soybean ending stocks.